When it comes to finance, Americans have had a few rough years. From rising interest rates to monumental inflation rise, the recent few years have been quite tumultuous for the United States of America. However, this could change in 2024. According to experts, 2024 can be an eventful year for Americans and their finances.

We are almost halfway through the year and have consulted various researchers and experts about what the rest of the year may hold for Americans. Let’s take a look at a few predictions to get a clearer picture of the American financial scene.

- Most Popular Financial Trends in 2024

- Key Takeaways

- Most Effective Personal Finance Stories from 2023

- Resumption of Student Loan Repayments

- Inflation Curbs but Rising Prices are Still a Concern

- Mortgage Rates Hit a Record 23-year High

- The Fall of the Silicon Valley Bank

- IRS Delayed Strict Online Selling Rule

Most Popular Financial Trends in 2024

Take a look at the best financial trends in 2024 that could change the financial scene of American finance in the coming years.

Federal Fund Rates Likely to Decrease

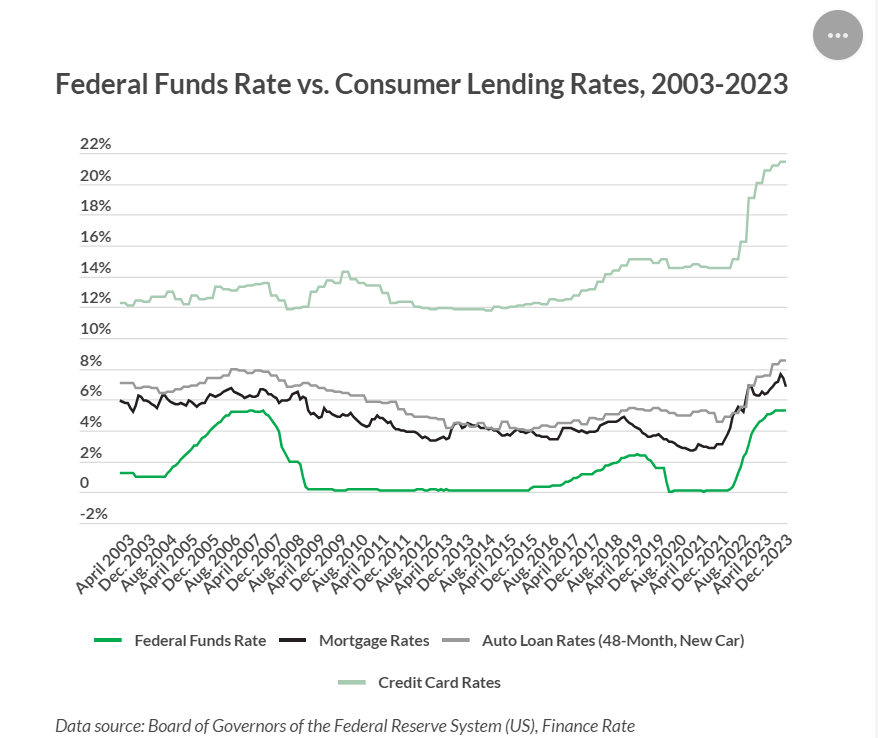

The federal funds rate is the benchmark at which lenders borrow money to finance banking and lending. To combat the rising inflation, the Federal Reserve started raising interest rates in March 2022.

At the start of the operation, the interest rate stood at 0.08%. However, by August 2023, the rate reached a whopping 5.3%, a monumental increase of 562.5%. This rate increase led to an increase in consumer lending rates like home loans, mortgages, credit cards, and more. It led to an increase in loans for people who borrowed purchases at the time. Moreover, with rising inflation rates, the expenses compounded and became detrimental to the finances of an average American citizen.

However, the last interest rate increase happened in July 2023 and it has remained constant since then. Federal Reserve Chairperson Jerome Powell said that the rates would not go down until the target rate of 2% inflation has been achieved.

But, many financial experts think that the Fed will start decreasing interest rates in 2024. The general consensus remains that the Fed will drop the rate by 1.5% in 2024, reaching a rate of 3.8% by the end of the year.

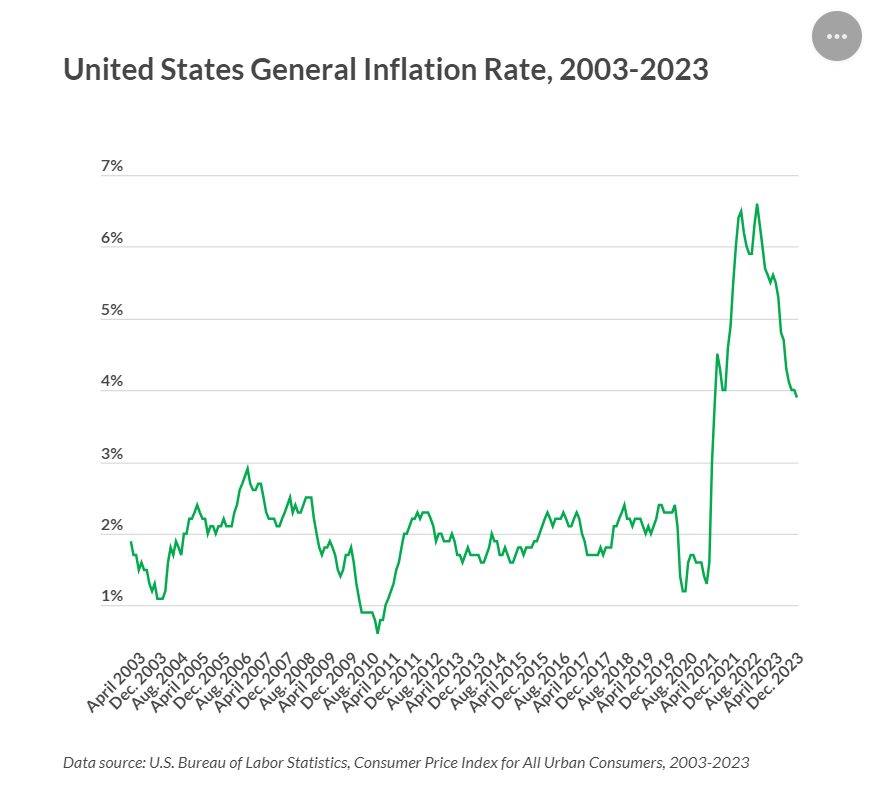

Inflation is Expected to Go Down

The rise of interest rates had an effect on lowering inflation, to some degree. Inflation peaked at 9.1% in mid-2022 but started decreasing by mid-2023, a year after the interest rate hikes began. As of now, inflation stands at an estimated 3.4%.

According to experts, this trend will continue in 2024 and the average predicted inflation rate by the end of 2024 is around 2.5%

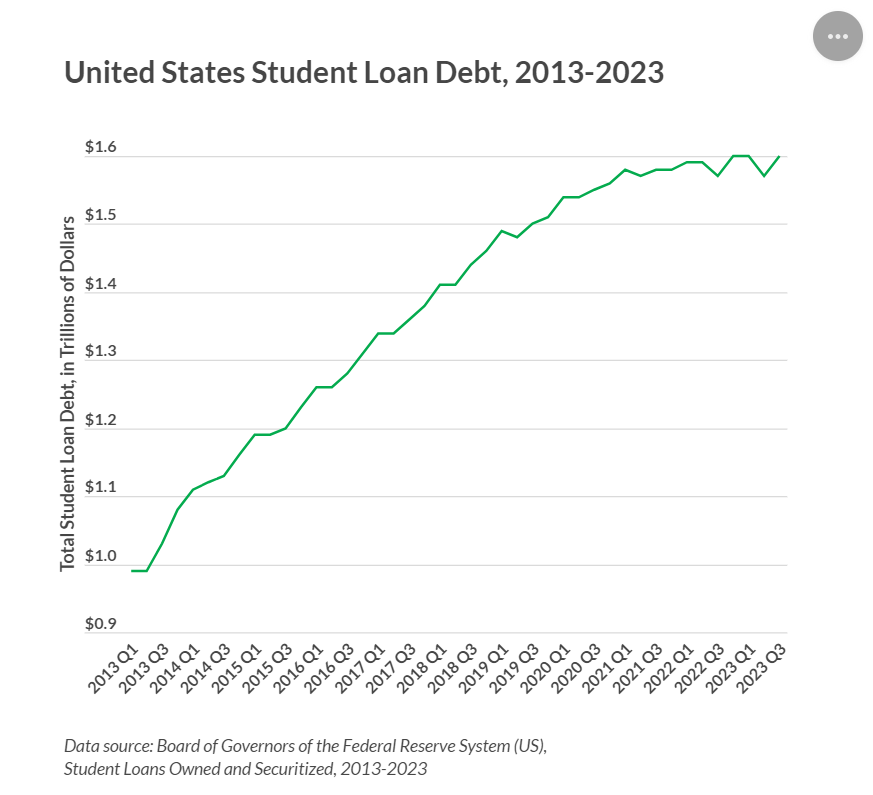

Student Loan Debt Relief Will Be a Lifesaver

Student loan debts are a growing concern for Americans and have been making the headlines for the past few years. With over $1.6 trillion in student loan borrowings, many government factions have been fighting back and forth over forgiving these loans.

The government started its forgiving program at the start of the year and thousands of people got relief from their debts. The Biden administration stated that it would forgive the debts of anyone who borrowed $12,000 or less and has been paying the debt for 10 years or more.

Read Also:- How to Get a Student Loan? Everything You Need to Know!

Presidential Elections Can Affect Financial Markets

The U.S. Presidential Election is scheduled for November 2024 and millions of Americans will head to the polls to vote for their presidential candidate. While there is not a significant change in market growth in election and non-election years, the picture is somewhat different when looking at year-on-year data.

The first half of the Presidential election year tends to be a bear market. However, things tend to escalate in the second half of the election year. The Dow Jones Industrial Average year-to-date performance is around -0.7% at the midpoint of election years. In non-election years this figure stands at 4.3%.

In non-election years, the Dow’s average second-half returns stand at 3%. But, this figure increases to 8.6% in the second half of election years.

Household Debt Could Reach Record High

Most of the expected financial trends of 2024 bring good news to Americans. However, there are also some challenges that could be detrimental to the country’s finances. The rising levels of household debt are expected to reach a record high in 2024.

At the start of 2024, the total household debt stood at $17.3, which includes everything from mortgages, home loans, and student loans to credit card debts. This figure is the highest in the history of the United States of America and is largely due to the rising interest rates.

While interest rates are expected to go down in the coming years, they would still be higher in comparison to pre-covid years. This means that paying those debts will be a herculean task for Americans.

Key Takeaways

- The federal funds rate is expected to go down by 1.5% by the end of the year. As of now, the interest rates stand at 5.3%.

- With a drop in interest rates, the commercial lending rates are also expected to drop.

- The government will start its student loan forgiving program, providing relief to millions of Americans suffering from rising interest rates.

- Record high household debts could complicate the American financial scene.

Most Effective Personal Finance Stories from 2023

With 2023 approaching its end, we have brought our top 5 stories from 2023 that had the biggest impact on the overall economy. From the feds lowering interest rates to high mortgage rates to student loan payments, there were plenty of stories in 2023 that influenced the economy and the general public.

The past year has been quite turbulent for the economy as inflation, rising interest rates, and more caused uncertainty. After the Federal Reserve raised interest rates to the highest level in 22 years, inflation began to curb, however, the general public is still concerned about the rising prices.

Here are some of the personal finance stories of 2023 that had the most significant impact on consumers and the economy.

Resumption of Student Loan Repayments

Student loan repayment resumed in October after a three-year pause that started during the pandemic. A ruling from the Supreme Court abolished the student loan forgiveness program proposed by President Joe Biden. This decision resumed student loan payments for 22 million people who owed an average of $275 per month on their student loans.

However, the Biden administration was quick to introduce a new income-driven repayment program after the first one was struck down by the Supreme Court. The Saving on a Valuable Education(SAVE) Plan sets monthly payments at 5% or 10% of a borrower’s income. Moreover, it also offers forgiveness for loan balances after 20 or 25 years.

As SAVE is similar to other IDR plans, students are not required to take any extra measures to sign up. Once enrolled, student’s payments can be cut in half and in some special cases, they might not need to make any payments at all. There’s an extended grace period from October 1 2023 to September 30, 2024, which ensures that borrowers(students) who miss payments won’t see any damage to their loan status or credit scores.

The White House estimates that the typical four-year public university borrower will save nearly $2000 a year with the SAVE plan, and 85% of community college borrowers are expected to be debt-free within 10 years.

Inflation Curbs but Rising Prices are Still a Concern

The Federal Reserve increased interest rates to 5.25%-5.50% in July to combat inflation. While the interest rate hike is effective in curbing inflation, prices have skyrocketed and the January 2023 Consumer Price Index(CPI) shows that prices were still 6.4% higher than a year before.

The interest rate hikes appear to be working, with the CPI showing annual inflation falling to 3.2% in October, lower than the expert’s estimates of 3.7%. Other inflation measures also moved lower as the Personal Consumption Index(PCE) fell as low as 3% in June. According to gas price website GasBuddy, gas prices have also fallen for 10 consecutive weeks.

However, rising prices are still a major concern for consumers. The Michigan Consumer Sentiment Index decreased for 4 consecutive months, with households reporting that they expect inflation to worsen over the next 12 months. Another measure of consumer optimism, the Consumer Confidence Index, showed that consumers expect inflation to rise to 5.7% over the next 12 months.

At the end of the year, many central banks have paused the incessant interest rate hikes, with the European Central Bank, the US Federal Reserve and the Bank of England all holding rates steady in early November.

Mortgage Rates Hit a Record 23-year High

Increasing mortgage rates has had a terrible impact on the real estate industry. Anyone in the housing market in 2023 knows the horrors. The effect of rapidly increasing mortgage rates on the market was everywhere, from buyers being priced out of the market to sellers holding onto properties they purchased with favourable rates.

Mortgage rates increased to 8% in 2023, a record high in 23 years. Rates revolved around the 8% mark for most of October before slowly decreasing in mid-November. As the Federal Reserve continued to increase interest rates in 2023, enacting four hikes in a single year, mortgage rates also rose simultaneously.

Starting the year at 6.5%, the average mortgage rate has risen almost 1.5% since then. It has more than doubled since the start of 2022. Higher mortgage rates decreased the volume of mortgage applicants to their lowest point in 28 years as fewer homebuyers chose to indulge in higher costs of borrowing.

Read Also:- Boeing Stocks Fall After 737 MAX Inspections For Possible Loose Bolt

The Fall of the Silicon Valley Bank

In March 2023, the Silicon Valley Bank collapsed suddenly and sent shockwaves through the US banking markets. It kicked off a wave of fear when several banks failed and consumers feared whether their deposits were safe.

The fall of the SVB was just the first failure as Signature Bank was shut down a few days later. Soon after, the Swiss banking firm Credit Suisse went under, followed by the First Republic Bank.

The crisis raised questions about the security of the deposit system. While the Federal Deposit Insurance Corp. (FDIC) insures accounts up to $250,000, some individuals and businesses at the institutions had larger accounts, putting them in jeopardy of losing deposits.

IRS Delayed Strict Online Selling Rule

The IRS once again delayed a new set of rules that affect individuals who sell items online on websites like eBay, and Etsy, or use online payment systems like Venmo or GooglePay.

The current thresholds for the sale require the sellers to file a 1099-K form on more than $20,000 in revenue and 200 transactions. Until that decision, sellers had been facing a threshold of $600 for sales, including ticket reselling. The IRS has delayed the decision to implement the new tax rule for the second time.

However, online sellers can expect some stricter enforcement of the law in 2024, as the IRS announced that it will enforce a $5,000 threshold for online sales in that tax year.

Read Also:- Investment Banker Salary in the USA: What to Expect in 2024