In today's complex world of digital and modern finance, technological advancements are changing, and constant developments in personal finance can be seen. Banking and financial services have become crucial for a living; amongst this, an unseen barrier endures, which is the emergence of banking deserts. Banking deserts are not just arid regions; they are also areas where financial services are nonexistent.

For example, in a community where financial services are considered a luxury rather than a convenience, or where the nearest bank is located miles away, there are areas where people have no access to financial services and are financially illiterate.

In this blog, we will unravel the concept of banking deserts—the areas where financial services are considered a luxury. What is it like for a community to be deprived of fundamental tools for financial independence? How are these financial deserts caused, and how do people meet their financial needs? We will also explore the financial services used by people in banking desert areas.

What are banking deserts?

Desert credit financial or banking deserts are areas where bank branches are unavailable. Banking deserts are mainly found in rural areas. They occur mainly due to certain reasons, such as bank failures, population losses, increased demand for digital banking services, decreased demand for branch banking, and the closure of branches identified as underperforming.

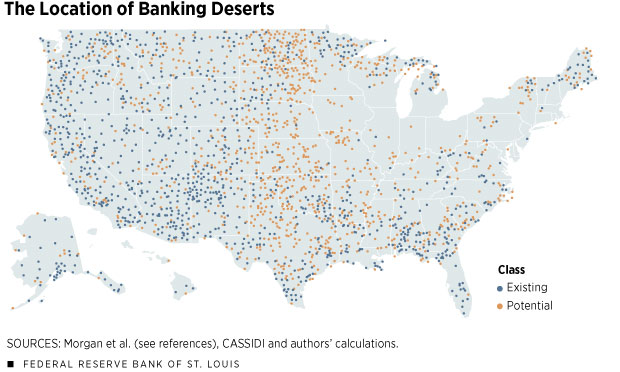

Banking deserts in the US

“Banking’s best deserts in the US” is a very common term around the world. 1,214 of the bank deserts in the US have been identified by economists working at the Federal Reserve Bank of New York, most of which are found in sparsely populated areas. Rural areas comprise the remaining 25% of banking deserts, with metropolitan statistical areas (MSAs) hosting 23% of them. Certain MSAs, like Boston and New York, don't have banking deserts.

There is a concentration of banking deserts in southeastern California, Arizona, and Nevada.

According to a report published by the Native Nations Institute, Native communities that are located in areas devoid of banks and banking services face numerous unique difficulties. The report, which details the expansion of capital access in Native American communities since 2001, reveals that in 2001 approximately half of the reservations surveyed lacked a financial institution within a 30-mile radius of their community.

The average distance (in a straight line) between tribal communities and financial institutions has decreased, according to more recent statistics, with the distance now standing at 12.2 miles. Still, this is more than ten miles that separates an area from being considered a banking desert.

This indicates that a variety of unique difficulties are still faced by tribal communities, thanks to the unavailability of bank branches.

Causes of Banking Deserts

The following reasons contribute to banking deserts:

The 2008 financial crisis

The financial crisis of 2008 shook the entire financial market. Many banks closed as a result of the 2008 financial crisis and its aftermath. According to the NCRC (National Community Reinvestment Coalition), between 2008 and 2016, 6,008 of the 95,018 branches were closed, leading to the establishment of 86 new banking deserts in rural areas. These banking deserts disproportionately impacted minorities; 25% of all closures took place in census tracts with a majority of minorities.

Economic Factors

There may be less financial incentive for traditional banks to open branches in rural areas with low population densities. In an area with a low population density, the expenses associated with running and maintaining physical branches might exceed the potential profits. Traditional banks might view them as less profitable areas due to lower income levels. Financial institutions might be reluctant to open branches in areas where the population has a modest income.

Market Forces

Market forces have a great impact on branch closures. Banks tend to steer clear of sparsely populated areas because the expenses associated with opening and operating a physical bank branch may exceed the potential earnings.

Financial institutions may cluster in more affluent or densely populated areas due to intense competition, leaving less economically attractive areas underserved.

Traditional banking institutions may find it difficult to attract themselves to areas with significant wealth disparities. Banks might favor locations where there is a greater concentration of wealthy clients. Certain communities may receive inadequate financial services or be shut out of mainstream financial institutions as a result of historical discrimination and systemic injustices.

Geographical and Infrastructural Reasons

Geographic isolation in some places can make it difficult and expensive for banks to open and operate branches. Access to banking services can be hampered by inadequate transportation infrastructure, especially in rural or isolated areas. Therefore, due to diminished market access, rural areas are more vulnerable to becoming banking deserts.

Some places lack transportation facilities and road structures, which makes it difficult for people to reach the bank branches.

Natural features such as mountains and rivers also affect the construction of banks, as it makes it difficult for banks to construct a bank branch there.

Demographic Factors

An area's employment trends and age distribution, among other demographic factors, can affect how much demand there is for banking services. An area with a higher proportion of elderly residents, for instance, might require different banking services than one with a lower population. Also, business cities tend to have more branches than farming-prone cities.

Technological Shifts

The ease of digital banking has increased the demand for online banking, which has resulted in a decrease in traditional banking services. Traditional banks can offer banking services without opening any branches in rural areas. This could save banks from running branches at a loss while at the same time helping rural people with banking services. In many countries, digital banking is seen as a replacement for traditional bank branches.

Urban vs. Rural Disparities

Traditional financial services are more likely to be located in densely populated areas, resulting in urban and rural disparities. Rural areas lack the services and resources to build financial services and banks. Most of the rural people are also not so well educated, which further results in no benefit for building banks and financial institutes.

Implications of Financial Deserts

There are various implications for bank deserts. They can affect people individually, in their communities, and in the economy as a whole. Among the most important ramifications are:

Limited Access to Financial Services

Lack of financial services leads to financial exclusion, which leads people to miss out on financial services such as loans, savings accounts, and cashing checks. Although there are online banking desert financial services available, the exclusion of people from bank branches leads to hindrances in managing finance, saving up, and accessing credit and loan facilities. Although digital banking can fill up the space, we are still very far away from complete access to financial services.

Low-cost credit unavailability

Due to the reduced financial services, it becomes difficult for people in banking deserts to have a source of credit, resulting in a low credit score. The people start relying on other resources and pay a higher rate of interest in return. Some of the research shows that people who take on a conventional-rate mortgage pay 5% more on their borrowings, which only makes their economic condition worse. Thus, for such a commodity, desert credit financial is a luxury.

Reduced Economic Opportunities

Limited access to financial services affects the establishment and development of small businesses and local businesses. Due to the low financial services, people are not able to take out loans to grow, develop their businesses, and hire more staff. This results in a community’s slower economic growth and greater unemployment rates.

The lack of desert financial services also impacts the growth opportunities for professionals. It gets difficult for people to get funding for graduation or skill-building courses that can improve their careers.

Lack of financial services also leads to the underdevelopment of society and the community. The building of infrastructure like public spaces, schools, and hospitals may need to be improved. This hinders the overall development and impacts the general well-being of a community.

Social and economic marginalization

Lack of desert financial services can worsen a cycle of poverty by making it difficult for locals to obtain the capital they need to get out of a bad financial situation. Social and economic marginalization may result from this, which could have a long-term negative impact on community well-being.

People who live in banking deserts may be more susceptible to financial shocks like unanticipated medical costs or job losses because they lack access to savings accounts or reasonably priced credit. The community's sense of economic marginalization is sustained by this financial instability.

Low financial literacy

Growing up in an area with no banking services leads to low financial literacy as people are deprived of the services and are never able to experience them. This can have a dangerous impact on their financial health, budgeting, and credit scores.

In a Money Geek survey of Native Americans, 75% of respondents said they couldn't come up with $2,000 for emergency expenses, and 63% said they couldn't pay their bills.

Difficulties with Education and Property Ownership

It may be difficult for students in banking deserts to obtain educational loans, which will limit their options for further education and employment in the future. Where students from developed cities move abroad for studies, students from rural areas cannot even pursue studies. Similarly, it may be challenging for locals to buy homes due to a lack of access to mortgage services, which can restrict their capacity to accumulate equity and create financial stability through homeownership.

Desert Financial Services

Due to the lack of financial services in the banking deserts, the following are the alternatives used to meet people’s financial service needs:

1. Desert Financial Credit Union

Desert Financial Credit Union is a credit union with 47 branches located in Phoenix, Arizona. Its service center serves the countries of Coconino, Gila, Maricopa, Pinal, and Yavapai, as well as the state of Arizona as a whole. Desert Financial is Arizona's largest credit union, managing assets close to $8.5 billion as of October 2022.

This Financial Credit Union offers a variety of financial services like savings and checking accounts, savings certificates, IRAs, home equity loans, mortgage loans, and business loans for people living in banking desert areas.

2. Check Cashing Services

People can check cash without the need for a bank account. This service has a high fee. People who use this method may get instant money, but they miss out on banking services such as financial savings and credit-building advantages.

3. Payday Lenders

Tribal payday lenders give loans for the short term and have a higher rate of return than banks.

They are designed for accessing cash quickly in case of an emergency or an immediate expense. They usually result in damaging people’s credibility even more, making the situation worse. Therefore, this service is often not recommended.

Conclusion

In conclusion, banking deserts are a curse to tribal areas and make it more difficult for people to carry out basic financial needs like depositing checks, taking out loans, and paying bills. Banking deserts enlarge the gap between high-income society and low-income society. Although banks such as JPMorgan Chase are planning to open new branches in moderate-income neighborhoods, low-income tribal areas need to wait a little longer for their first bank branch.

Digital banks can be of a rescue to this. They are crucial for people living in banking deserts, as they can help fill the gap between people and their financial service needs. Digital banks are also more fee-friendly and offer high interest rates on deposit accounts.

There are many disadvantages and impacts of the lack of financial services on people, both economically and financially, but getting financial literacy and using digital banking are the only ways to improve the situation.

Frequently Asked Questions FAQs

There are a bucket full of reasons that contribute to banking deserts such as underperforming branches and loss of population. However, the rise of digital banking contributed the most. What’s more, 86 banking deserts were reported due to the financial crisis of 2008.

Even though banking deserts can be found in various corners of the country, they are mostly located in rural areas. For example, in the US, a large part of the southwest such as Arizona, southeastern California, and Nevada accounts for the most number of banking deserts.

People who reside in banking deserts do not have a bank account and rely on alternative financial services. For instance, check-cashing services, desert financial credit unions, or payday lenders. These alternatives offer high-interest rates and are much more inconvenient than banking services.